Part 2: Passive Portfolio Management

Market Meditations | June 3, 2021

We introduced Part 1 of our Portfolio Management Series on Monday. You can check out the full guide here or read this summary before continuing to Part 2:

- The inspiration of this series is the controversial finance book A Random Walk Down Wall Street.

- From emotional strain to liquidations, active trading is not for everyone.

- Further, there are difficulties associated with the necessary factors for successful trading: technical analysis, fundamental analysis and trading psychology.

- This makes the case for consideration of other alternatives to building wealth, such as passive income strategies.

Today, we will set about sharing various passive income strategies. As a disclosure, please note we are not financial advisors. The content in this newsletter is for informational purposes only. Nothing in this email is intended to serve as financial advice. Every investment and trading move involves risks. Do your own research when making a decision.

Diversification 101

Diversification is key to successful investing. It is a strategy that aims to mitigate risk and maximise returns by allocating investment funds across different vehicles, industries, companies and asset classes. Consider Diversification Dan:

- Without a diversified portfolio. It’s February 2020 and Dan’s portfolio is heavily exposed to stocks (shares in companies). Stock valuations are driven by the underlying cash flows and success of the companies. March 2020 and Covid-19 hits. Stocks suffer heavily: they need to implement lockdown and consumers start to spend less. Dan’s portfolio takes a heavy hit and he has to drastically change his lifestyle.

- With a diversified portfolio. Now imagine Dan had exposure to government bonds and some crypto assets as well as stocks. This time, in March 2020, his portfolio does take a hit from the troubles in stocks but his bond income (however small) remains consistent and his crypto assets (which act as an inflationary hedge) actually end up making him a good deal of money. He would fare better under normal circumstances but everything considered, he’s mitigated his risk to a large extent.

This example shows that when you diversify your investments, you reduce the amount of risk you’re exposed to in order to maximize your returns.

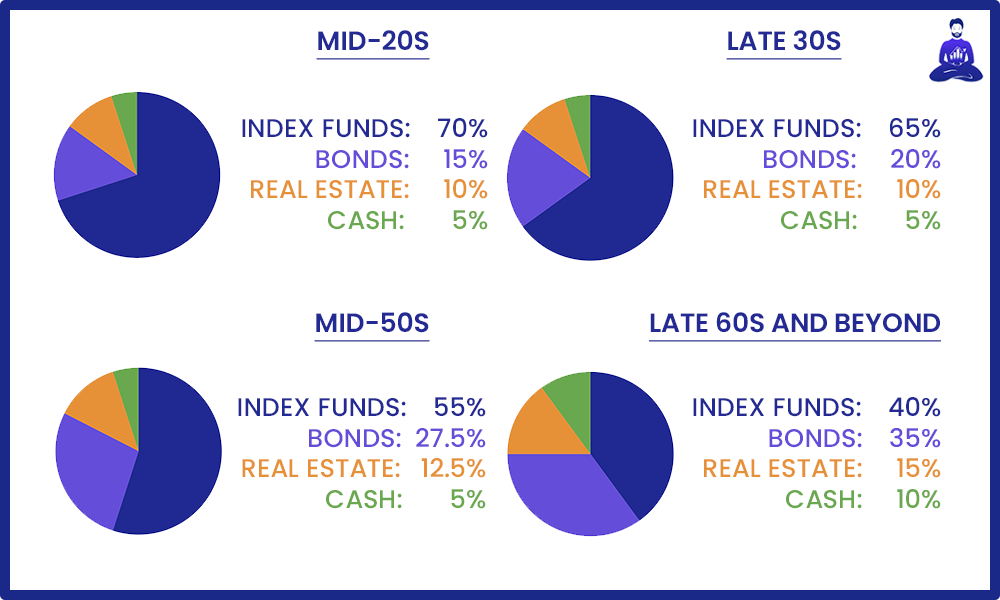

Lifecycle Guides

So what does a diversified portfolio look like? The book provides a few examples based on age.

Source: Random Walk Down Wall Street

Definitions:

- Index Funds. An index fund is a portfolio of stocks or bonds designed to mimic the composition and performance of a financial market index. Index funds have lower expenses and fees than actively managed funds. They follow a passive investment strategy and seek to match the risk and return of the market, on the theory that in the long-term, the market will outperform any single investment.

- Bonds. Debt securities issued by corporations, governments or other organizations.

- Real Estate. A class of “real property” that includes land and anything permanently attached to it, whether natural or man-made. You can invest in real estate directly by purchasing a home, rental property or other property, or indirectly through a real estate investment trust (REIT).

- Cash. A legal tender that can be used to exchange goods, debt, or services.

Accessing these assets: A Random Walk Down Wall Street provides an address book with lots of different options for getting exposure to various asset classes.

Overview:

- For those in their twenties, the portfolio is more aggressive. The idea being that at this age there is lots of time to ride out the peaks and valleys of investment cycles and a lifetime of earnings ahead of you.

- As investors age, the idea is that they start cutting back on riskier investment and start increasing the proportion of the portfolio committed to bonds. The allocation is also increased to REITs that pay generous dividends.

- By the age of fifty-five, there is a transition to retirement and moving the portfolio toward income production. The proportion of bonds increases.

5 Core Principles

The above charts are a guideline. There are 5 core principles that underpin any portfolio allocation strategy:

- Risk & Reward. Risk and reward are related. Risk is defined as the volatility of an individual investment. Whereby volatility is measured by how much the return typically differs from its expected value. You must always first determine your own risk tolerance.

- Length of hold time decreases risks. The longer you hold on to an investment, the more likely it will perform according to its expected value. Determine your time horizons when you are assessing risk.

- Dollar cost average. This means investing the same fixed amount at regular intervals. 10% of your salary in an investment each month for example. Always give your entry method and approach consideration. For more on dollar cost averaging, check out our video guide.

- Define your capital. Determine how much money you can invest and importantly how much you can lose. If losing your investment means you will need to drastically change your lifestyle, you might want to downsize your risk. Similarly, if your investment exposure is impacting your sleep and health you may want to “sell down to the sleeping point” as JP Morgan once suggested to a friend. To help determine how much capital to invest, check out our emergency fund article.

- Rebalancing. Rebalancing and somewhat decreasing your exposure to over performing asset classes can reduce risk and possibly increase returns.

What About Crypto?

We’ve mainly referenced non-crypto investments in today’s article but the point still stands with crypto investments too. Let’s apply the 5 core principles to crypto.

- Risk & Reward. Crypto is a new technology that less than 2% of the world uses. This presents us with large upside potential and a lot of risk. This makes it suitable for investors with a higher risk tolerance, especially those earlier in the life cycle.

- Length of hold time decreases risks. Now historically anyone who’s held bitcoin for a long time has done pretty well. However the sample size for this is small. We view bitcoin as a binary asset that will either continue to grow in adoption and price or fail. Hence having a long time horizon makes it more probable we realize it’s potential upside.

- Dollar cost average. This will diversify our timing risk with Bitcoin. Most people can’t identify the best time to buy bitcoin, DCA means they don’t have to.

- Define your capital. The information mentioned above should help us define the most suitable amount of capital to Bitcoin.

- Rebalancing. This technique can be especially useful to take advantage of and benefit from bitcoin’s volatility.

For more on passive income strategies in crypto, check out our Passive Income article.